Who could have imagined we would start with the spread of a virus, add some political election turmoil, and now we have an OPEC price war. Wow!

Although we can’t control viruses and oil price wars, there are many things we CAN do to prepare for this bear market or recession. Here are five things to do in order to not freak out and bring peace to your financial life:

1. Stop watching the news and start reading it.

It’s important to be informed. However, the 24-hour news cycle, selling fear and anxiety, is at an all-time high. Instead of watching TV or sensationalized videos, read your news from reputable sources. This will help reduce your emotional reaction while helping you stay knowledgeable and informed. Call us if you would like suggestions of reputable sources.

2. Evaluate your personal budget and balance sheet.

For those of you who have very low debt and a sufficient emergency fund, you can rest easy. Even if you are laid off or furloughed, you will have sufficient cash to prevent you from raiding your retirement funds. If this is not you, consider the following:

- Develop a spending plan to eliminate all short-term, high-interest debt as soon as possible.

- Refocus your spending on necessary items only.

- Increase your emergency savings through automatic payroll deductions.

- Avoid new purchases unless cash is available.

3. Consider refinancing your mortgage.

A good friend and client recently refinanced his mortgage to a 15-year 2.56% interest rate. In early March 2020, saw mortgage rates fall to the lowest level in almost 50 years. That’s a game-changer for retirement planning!

4. Stay in the fight.

You don’t have to be invested in 100% equities all the time but staying in the market in some capacity is required to capture the long-term market gains that are available to all of us. It’s been shown that leaving the market only to return later may diminish your returns significantly. In fact, if you miss out on just a few of the positive days in the market, your long-term stock averages could suffer tremendously. You have to manage risks in the stock market – not avoid them completely.

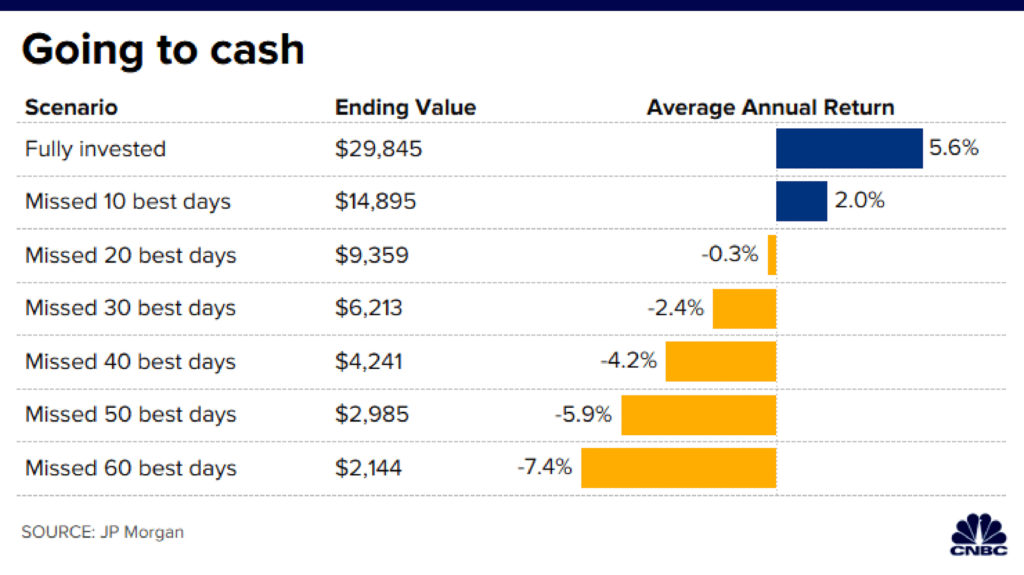

The chart below shows how $10,000 invested in the S&P 500 index, for the 20-year period of 1999 through 2018, would have performed under various scenarios.

If the $10,000 remained fully invested, it would have grown to $29,845 with an average annual return of 5.6%.

By comparison, missing out on just the best ten days in that time period would have reduced the growth of the initial investment by more than half. After 20 years, that $10,000 would be just $14,895 with a 2% average yearly return. So we recommend that you stay put.

5. Focus on your goals and your investment time horizon.

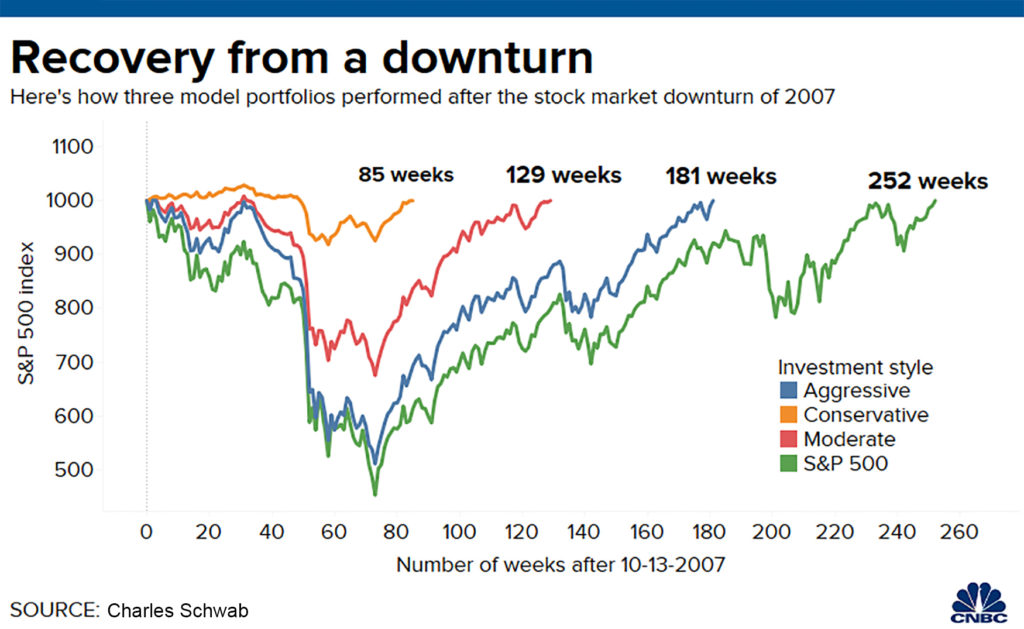

Remember, the money you will need in one to five years is not at risk in stocks. It’s only a paper loss until you sell the stocks. You wouldn’t sell your house or rental real estate property just because the price declined so why would you sell your stocks? Furthermore, more conservative portfolios recover faster from downturns than aggressive ones. For example, according to Charlies Schwab, a portfolio with more than 70% stocks and the rest in bonds took more than two years to recover from the 2008-financial crisis, compared with just seven months for a portfolio with more than 70% in bonds and the rest in stocks.

As always, we’re here for you. This stuff can be unsettling. Don’t hesitate to reach out to us with your questions and concerns.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this article will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Moreover, you should not assume that any information or any corresponding discussions serves as the receipt of, or as a substitute for, personalized investment advice from Leading Edge Financial Planning personnel. The opinions expressed are those of Leading Edge Financial Planning as of 03/12/2020 and are subject to change at any time due to the changes in market or economic conditions.

{kind=link}