Conventional and FHA loans are generally available to anyone with a qualifying credit score. There is another type of loan, guaranteed by the United States Department of Veterans Affairs, available to U.S. veterans, those currently serving in the U.S. military, reservists and select surviving spouses (provided they do not remarry) that can be used to purchase single-family homes, condominiums, multi-unit properties, manufactured homes and finance new construction. Known as a VA loan, it allows eligible borrowers to purchase a home with as little as $0 down which can be a very attractive option for qualified buyers. A VA loan is not originated/processed by the Department of Veteran Affairs; most mortgage lenders are able to originate the loan and the Department of Veteran Affairs simply provides the guarantee. Because a VA loan is guaranteed by the government, borrowers are not required to pay any type of monthly mortgage insurance regardless of their down payment.

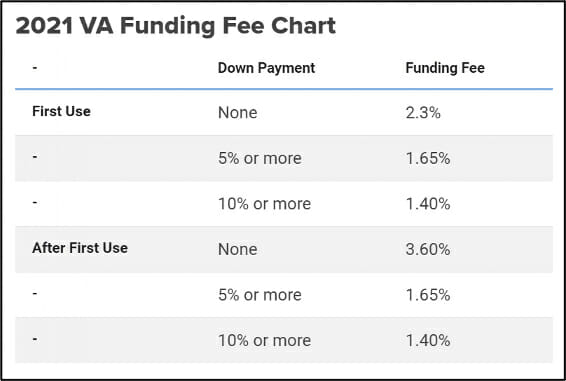

When an eligible borrower applies for a VA loan, one of the first steps the loan originator will do is to obtain the service member’s Certificate of Eligibility, or COE. VA-approved originators have access to the VA system and can generally obtain the COE in a matter of minutes. Borrowers themselves may also obtain their COE through the VA’s eBenefits portal online or by submitting VA Form 26-1880 via mail. For surviving spouses, additional documentation may be required to obtain a COE. An important piece of information on the COE is whether or not a “funding fee” must be paid as well as the amount of the veteran’s “entitlement” which is simply a measure of how much the VA is able to guarantee. While a VA loan does not have any monthly mortgage insurance, think of the funding fee as an upfront payment of mortgage insurance. This fee goes directly to the VA and can be financed into the loan, paid out of pocket, or in the case of a purchase, you may be able to ask the seller to pay it on your behalf. Not everyone is required to pay this funding fee; generally, service-connected disabilities may allow a funding fee exemption. For those who are not exempt from paying the funding fee, the percentage depends on the amount of down payment being made, as well as if it’s the borrower’s first or subsequent use of their VA benefits:

VA IRRRLs (Interest Rate Reduction Refinance Loan – a very streamlined refinance process) all carry a 0.5% funding fee unless the veteran is otherwise exempt from the funding fee.

The VA doesn’t have a minimum credit score to qualify for a VA loan, though lenders may have overlays that impose certain requirements. Most lenders will require a minimum 620-640 credit score. One qualification criterion unique to a VA loan is the requirement for “residual income” analysis by the lender. Residual income is essentially “left over” income each month after all expenses are paid. By requiring residual income analysis, the VA ensures there is a cushion for increased debts or other types of temporary financial emergencies. VA purchase loans also require an appraisal by a VA-designated appraiser.

Beyond the few unique requirements of a VA loan, many other aspects are similar to a conventional or FHA loan. The lender will require pay stubs, W2’s, asset documentation, and tax returns (for self-employed borrowers).

A veteran who has used their benefits to previously purchase a home, may have entitlement left to purchase another one. If a home was previously purchased using VA benefits, there may still be entitlement available to purchase a new home. The lender will calculate the maximum entitlement available considering the following:

- If a previous home was purchased using a VA Loan, and that loan was paid off by the new owners, the full entitlement may have been restored.

- If a borrower sold their home and allowed the purchasers to assume the VA Loan, then the borrowers may have the full entitlement restored if one or more of the purchasers were also veterans.

- If a borrower owns a home and is renting it out, they may be able to purchase a new home using partial entitlement.

If you’re eligible for a VA loan, it can be a very good option to consider. Zero or minimal down payment, no monthly mortgage insurance, and the option to be able to refinance using a VA IRRRL all make considering a VA loan worthwhile. Your mortgage lender should be able to compare different loan products, including a VA loan, to help you make the best decision possible.

{kind=link}