")

")

It’s shaping up to be a fascinating year in the markets already! New president and administration, government layoffs, airline layoffs (SWA), tariffs roiling the U.S. markets and so on.

So, what should you do? How might you invest right now to make sure you’re going to be okay whether you are a brand-new first officer or you’re preparing for retirement this year? We’ll get to this in a moment, but first…

A client and friend texted me the other day: “A retired banker is running around saying market is getting ready for a correction bigger than 2008. Because of tariffs and the new global economy. What should we do?”

Here are a few other headlines that are sure to get your attention:

- Ray Dalio, billionaire and founder of Bridgewater Associates hedge fund, predicts a U.S. debt crisis “Heart Attack” within three years

- From the Federal Reserve Bank of Atlanta:

- The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2025 is -2.8 percent on March 3, down from -1.5 percent on February 28. After this morning’s releases from the U.S. Census Bureau and the Institute for Supply Management, the Nowcast of first quarter real personal consumption expenditures growth and real private fixed investment growth fell from 1.3 percent and 3.5 percent, respectively, to 0.0 percent and 0.1 percent.https://www.atlantafed.org/cqer/research/gdpnow

- Many of you may know that one of the many criteria for a recession is two consecutive quarters of negative GDP. It appears that we’ll have at least one quarter of negative GDP by the time you read this article.

- Chief Economist at Redfin, author and former Academic Advisory Council Member of the Federal Reserve Bank of Dallas, Daryl Fairweather, Ph.D., recently posted the following on X (formerly Twitter):

- “Unless we all wake up from this collective tariffs nightmare, the reality is recession. Recession with inflation which is called stagflation. It’s the worst kind of recession, because people lose their jobs and prices stay high along with interest rates.”

At the beginning of every year and at every point in time within the year there are scary headlines and many people making forecasts that make you want to remove your money from the stock market and get off this crazy roller-coaster ride called investing.

There will never be a time when there is an absence of headlines, events or forecasts that makes you not want to invest. I know that’s a lot of double negatives but it’s true. To quote Daryl Fairweather, Ph.D. again, she says this about forecasting:

“What most people get wrong about forecasting: The thing that almost no one understands about forecasting is that almost all forecast models are unfalsifiable. So that means that if I say there is a 10% chance that it’s going to rain tomorrow and it doesn’t rain, you can’t prove whether or not I was wrong. If it does rain, you can’t prove whether or not I was wrong, because I said there was at least some probability that it would rain or not rain. And that’s how almost all economic forecasting works…”

Let’s continue with the weather-forecasting theme. Warren Buffett said he hasn’t read an economic or market forecast in over 25 years. “There is no value, they only make weatherman look good.”

Now back to the focus of this article; what does this mean for you and what should you do about it?

Here are a few (less-than-ideal) options:

1. Invest in what did the best last year. The S&P 500 was up almost 25%! Surely that would work going forward.

2. We could look to the retired banker or other prognosticators for advice and simply do what they say. There are some really smart people out there shouting Armageddon from the rooftops already. It seems like if we just did what they said, we’d be okay.

3. Why not just ask Google, Siri or even ChatGPT? Those sources will consolidate all the loudest voices – I mean, best advice.

What makes investing so hard is that we have no idea what the impacts of tariffs will be. We have no idea if the investment that did well last year will continue to outperform all other areas of the global market. And we have no idea what a retired banker means when he says, “the new global economy.” In fact, the banker doesn’t know either, but it sounds smart.

I’m not sure who gets the credit, but one of my favorite quotes on investing is, “The best investors in the world must be prepared for multiple outcomes.” In other words, nobody can accurately predict the future. Therefore, we must invest in multiple strategies at once. Some investing strategies may do really well, depending on how the unknowable future plays out, and other strategies or investments may do poorly. Only in hindsight can we know which ones will thrive.

Below are three steps to ensure that you are a successful investor whether you are a brand-new first officer, or you are on the cusp of airline retirement.

- I always feel like recommending diversification is such a disappointing strategy.

I just assume everyone is tired of hearing about it. Plus, it’s really not a fun way to invest. In fact, my second favorite investing quote is, “You know you’re properly diversified when you want to throw up!”

Even though you may want to throw up, or fire your advisor, diversification is what allows us to prepare for multiple unknown outcomes at once.

Last year the S&P 500 returned nearly 25% and a growth-focused index fund almost returned 35%. It’s very tempting to try to invest in yesterday’s returns. In fact, some experts call this, “investing in the rear-view mirror.” I will never criticize any of those strategies because they might work for you. We’ll only know in the rear view!

Interestingly, both investments I mention above are in negative territory as of the writing of this article (early March) and an international index fund is one of the better performing investments so far this year with a year-to-date return of approximately 10%. (Schwab International Equity Index Fund)

- Maintain focus on your investment game plan and do not use headlines, forecasts or your Google feed to influence your investing decisions.

It sounds obvious but this is really hard. We are bombarded by social media influencers, experts on the news, and even political influences that make us want to change what we’re doing. In fact, this influence is happening without us even knowing it. It’s almost impossible to turn off the noise. The best thing we can hope to do is acknowledge the noise and treat it as entertainment if you enjoy that sort of content.

Can you imagine if you acted on or followed the advice of the following article headlines?

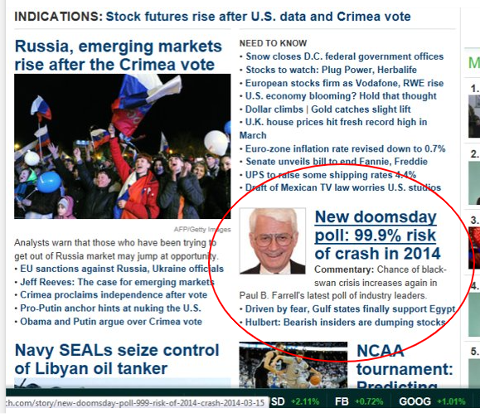

The screenshots below are from MarketWatch.com.

- March 2014. “New doomsday poll: 99.9% risk of crash in 2014.” There were some scary events going on for sure in 2014. Interesting to see the Russia/Ukraine war was brewing long before 2022. And they made a movie about the headline in the bottom left!

- The second MarketWatch headline screenshot is from a few months later in July 2014. John Hussman is a highly respected economist and head of Hussman Strategic Advisors.

By the way, the S&P 500 returned nearly 14% in 2014!

Neither John Hussman nor Paul B. Farrell lost any money from writing those articles for MarketWatch in 2014. Both are still in the business of writing books and managing investments. However, if you took action based on their articles, you could have lost a significant amount of your retirement nest egg.

- Understand the quality of your information, where it comes from and use extreme caution for the confirmation bias.

Here’s a definition of confirmation bias from Britannica.com: Confirmation bias; people’s tendency to process information by looking for, or interpreting, information that is consistent with their existing beliefs. This biased approach to decision making is largely unintentional, and it results in a person ignoring information that is inconsistent with their beliefs. These beliefs can include a person’s expectations in a given situation and their predictions about a particular outcome. People are especially likely to process information to support their own beliefs when an issue is highly important or self-relevant.

My Google and YouTube feeds are filled with financial articles, sports scores and headlines. Google and Meta design algorithms to keep me scrolling through Google and using YouTube as a go-to source of information or even stalking my friends on Instagram. And I kind of like it! (Full disclosure, I’m not on Instagram and I know nothing about it. So, I’m not actually sure you can stalk your friends on Instagram!)

There’s nothing inherently wrong with these algorithms because Google wants to get the content in front of me that I like to click on the most. This is how they get their advertisements in front of me so they can get paid by their customers.

However, just type this in your Google search if you want to learn why you should use caution and how those algorithms might feed your confirmation bias; “Do Facebook and Instagram have algorithms that promote confirmation bias?”

Here’s one sample from SkillFloor.com’s article “Impact of Social Media Algorithms on User Behavior”:

“Social Media Algorithms tend to show you content that aligns with your existing beliefs and opinions. While this can be comforting, it also creates echo chambers where you only see one side of an argument. This confirmation bias can lead to a skewed perception of reality and hinder critical thinking.”

I believe that if you work these three principles into your investing philosophy it will go a long way towards ensuring a successful investing experience regardless of where you are on your investment and professional-pilot journey.

In summary, it takes a lot of discipline to maintain your portfolio diversification. Do not listen to predictions or forecasts, regardless of the source. There are studies that show you may be better off flipping a coin to predict the future of economic and financial markets. And finally, use extreme caution and discretion about the source of your financial information—it's everywhere and most of it doesn’t apply to your financial situation!

Charles Mattingly, MBA, CFP® | CEO & Lead Planner

Leading Edge Financial Planning

865-240-2292 Office

865-328-4969 Cell/Text

Hopefully, you found this article interesting and helpful. If you have any questions, contact us at 865-240-2292 or Charlie@leadingedgeplanning.com.

Also, please tell us if we can help you on your journey to financial peace and prosperity! Click here to sign up for our newsletter or click here to schedule some time to chat about your circumstances in more detail. Also, check out our Pilot Money Guys podcast where we regularly discuss these types of financial topics along with some fun airline news updates and interesting guest interviews. Even the editor and founder of Aero Crew News – Craig Pieper!

Leading Edge Financial Planning LLC (“LEFP”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where LEFP and its representatives are properly licensed or exempt from licensure. For additional information, please visit our website at www.leadingedgeplanning.com.

The information provided is for educational and informational purposes only and does not constitute investment advice, and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status, or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance, and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

{kind=link}