")

What's up with recent stock market volatility and what should you do about it? January 2022 was the worst month in the stock market since March 2020. By the time you read this article, the markets may have recovered and gone higher, or perhaps new and unexpected news may have caused the markets to tank even further. Is this something we should be worried about or fear?

We fear the wrong things:

When I flew F-16’s for the Air Force, I worried about and feared the wrong things. Looking back now, I’m amazed at how much energy and effort I put into the things that really didn’t matter much. Instead of focusing on executing the specific tactic that would allow us to accomplish our mission that day, I was consumed with worry and uncertainty about how the instructor might be grading my performance.

I remember one upgrade ride particularly. After we landed, I was so wrapped up with how bad I thought my performance had been that I failed to focus on the upcoming debrief and what we could have learned from that sortie – you know, the really important stuff! It’s embarrassing to look back now, but experience brings a perspective that is difficult to recognize as a young fighter pilot.

As it turns out, I’m not the only one worried or fearful of the wrong things. Sharks have a reputation for being people-eating monsters, however, sharks are only responsible for ten fatalities per year worldwide.1 On the other hand, eight deaths every day in the United States are caused by people texting while driving.2 My daughter loves to ride horses but unfortunately, she’s twice as likely to die while riding horses than by shark attack.3 I’m going to have a heck of a time convincing her to scuba dive with me because of her fear of what’s below the surface of the ocean. It turns out that scuba diving in the depths of the ocean is one of the safest places to be!

Similarly, normal stock market volatility is not the thing we should be concerned with or fear. However, this normal behavior of the stock market causes people to do irrational things that can hurt their long-term investment performance . . . and it’s really expensive!

Why is the stock market down this January 2022?

There’s plenty of stuff to be worried about for sure. Here’s a sampling of the headlines in mid-January from MarketWatch.com, January 23, 2022:

• “Nasdaq is down 11% in 2022 and poised for the worst start to a year since 2008.”

• ‘Godfather’ of technical analysis says the stock market could fall 20% or more, but don’t panic

• “Good luck! We’ll all need it” – Jeremy Grantham sees approaching end of a ‘superbubble.’

• “Omicron, high inflation, worried consumers: Just how bad is it for the economy?”

• “Weekend reads: Is this the end of the bull market for stocks?”

The experts responsible for these headlines are very intelligent people. However, I’m confident that if you invest according to these messages, you will NOT be a successful investor. And the data is on my side. (See graphic below.) The average investor reads these headlines, experiences fear and uncertainty, and sells their investments to prevent being a victim of the “superbubble,” the “worst start to a year since 2008,” the impending “fall of 20% or more.”

So, why the rocky start to 2022? Here are a few thoughts:

- The Fed’s December meeting minutes released on January 5 were more aggressive than the market anticipated. In other words, they warned of reducing long-term treasury purchases and multiple potential interest rate increases coming in the near future.

- The markets are worried about the Russia/Ukraine escalation.

- Inflation fears

- The 2021 year-end rally was probably an overshoot.

- Growth, tech-focused assets were overvalued to begin with. Furthermore, when interest rates rise, growth-focused stocks tend to do poorly due to their heavy reliance on cheap debt.

- The Omicron variant of COVID-19 continues to weigh on economic growth.

Okay, now what is the real reason the market is down year to date (Jan 31, 2022)? Two words; expectations and uncertainty. When it comes to the behavior (volatility) of the markets, it is not the actual event, news headline, Fed decision, etc. that has the biggest impact. What causes the most volatility is if the new information or the new event is different than what was expected.

Omicron is the perfect example of this. Mr. Market was expecting COVID-19 to be behind us in late 2021. When in fact a new strain was discovered in South Africa instead. Here's the direct quote from December 15, 2021, Federal Reserve press release (meeting notes.): “The path of the economy continues to depend on the course of the virus. Progress on vaccinations and an easing of supply constraints are expected to support continued gains in economic activity and employment as well as a reduction in inflation. Risks to the economic outlook remain, including from new variants of the virus.”

Focus on our mission as investors?

Just like my flying performance suffered during an upgrade flight solely due to me focusing on the wrong things, our investment performance and retirement success can also suffer from focusing on irrelevant short-term noise. One of our most common axioms in retirement planning is, “Do not let short-term events or news headlines affect your long-term plan.”

What is your mission as an investor? For most, it is to build wealth over the long term. Even if you are at or near retirement, you are a long-term investor. What the evidence shows us is oftentimes avoiding short-term discomfort in the stock market will work against the accomplishment of your mission. Know your mission and do the things that increase your odds of a successful mission. I believe one of the keys to success is to understand that it’s not about timing the market, but instead it is about time in the markets. According to the Putnam Investments graphic below, by staying fully invested over the past 15 years, you would have earned $22,270 more than someone who missed the market's ten best days. Furthermore, if you missed just the ten best days in the S&P 500 15-year period from December 2005 to December 2020 your annualized return would go from 9.88% to 4.31%!

Click here to see the full PDF presentation from Putnam Investments4

What is the biggest enemy of long-term investing success – Mission Accomplishment?

What happens when you heed the advice of experts and prognosticators who don’t know a thing about your personal circumstances or financial goals? In short, they win and you lose!

The main goal of online news sources, social media, etc. is to provoke strong, negative emotions so you’ll view their ads and buy what they’re selling. The same can be said for your favorite Twitter feed, 24-hour financial news source, or even someone on YouTube shouting Armageddon from the rooftops.

Large media sources and social media platforms spend gobs of money to employ expert psychologists and use sophisticated algorithms to feed you the news that will hook you. They also know that if they feed you the information you already believe to be true, you’ll be more likely to stay on their site for longer periods of time. Reading news that “agrees with you” is especially dangerous because it feeds your confirmation bias. Making you even more confident of the belief system you already had, which unfortunately may or may not be useful as it relates to your investments.

We all have seen real-world examples of far-out, but possible, belief systems that have cost investors tons of money. Is the end of capitalism possible? Absolutely! Could the United States become a communist country? Unfortunately, it’s possible. However tragic these events would be, they are not reasons to stop investing in globally diversified portfolios.

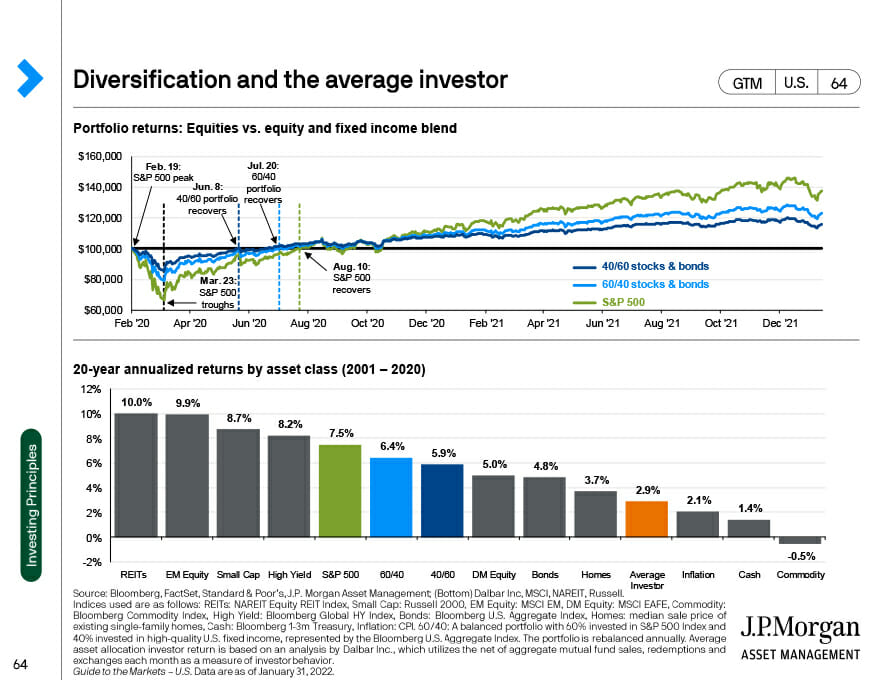

Every year JP Morgan Asset Management updates their record of asset class investment returns, and they include the average equity-investor performance along with it. Due to the roller coaster ride of emotions for the average investor, they tend to sell after markets have declined (sell low) and tend to re-purchase those investments afterthey have recovered (buying high). This repeated cycle of either chasing returns or trying to avoid the next crash leads to very poor investment performance. In fact, the average investor can underperform the actual performance of the mutual fund, ETF, or stock they are invested in.

From J.P. Morgan Asset Management “Guide to the Markets”5

“The top chart shows the powerful effects of portfolio diversification. It illustrates the difference in movements between the S&P 500, a 60/40 portfolio, and a 40/60 portfolio indicating when each respective portfolio would have recovered its original value at the peak of the market on February 19th from the market bottom on March 23rd. It shows that the S&P 500 fell far more than either of the two diversified portfolios and also took longer to recover its value. The bottom chart shows 20-year annualized returns by asset class, as well as how an “average investor” would have fared. The average investor asset allocation return is based on an analysis by Dalbar, which utilizes the net of aggregate mutual fund sales, redemptions, and exchanges each month as a measure of investor behavior. (Click here for the source graphic.5)

Maintain Aircraft Control!

Just like flying the airplane – success in investing in no secret or magic potion. It’s all about basic principles and discipline:

1. Maintaining aircraft control

2. Analyze the situation

3. Take appropriate action

4. Maintain situational awareness.

- Maintain Aircraft Control

- Turn off the financial news or Twitter feed that jacks you up! Trust me, you’ll be a happier person and your investments will do better because you won’t fear the wrong things or worry about things you can’t control.

- Fly the airplane first – focus on what you can control. On or about March 20, 2020, one client said to me; “There is no recession or market crash for those that have cash!” How true is that? I’m certainly not recommending holding cash in your investments while waiting for the stock market to fall, however, I do highly recommend maintaining a solid emergency fund of cash and low debt, so you’re not stressed out when the next crash comes along. We have seen how this can greatly improve quality of life as well as investment returns. Furthermore, you’ll be like a well-run airline (oxymoron) that is ready to take over market share when other airlines are trying to NOT go bankrupt.

- Analyze the Situation

- Understand that while the news, world events (e.g., Russia-Ukraine) could be terribly tragic and scary, they may not affect your investment plan. In fact, it probably won’t. The stock market has been through some pretty scary stuff and investors have managed to handily outpace inflation over the long term. (See the 1960s; The Cuban Missile Crisis, President JFK assassination, Martin Luther King, Jr. assassination, race riots, Vietnam War, etc.)

- Remember, you invest in the stock of companies, and they are amazingly good at making products we need and want. And therefore, making profits we can share during good times and bad.

- Take the Proper Action

- You must prepare for “The Crash”, before “The Crash.” Take the time to develop a well-thought-out financial plan and investment policy statement.

- Just like the simulator prepares you for the emergency before you ever face one in the airplane, thinking about what you’ll do when the next recession comes along could help you get through the event without real (only paper) losses in the stock market.

- Rely on your financial plan to help you understand “the why” behind your investment strategy. Having a game plan will help you understand what news headline or event might impact your financial goals.

- Be a humble investor. A good investor acknowledges that some things, such as short-term market gyrations, are unknowable. Furthermore, the best investors prepare for multiple outcomes (diversify!) and they are prepared to be wrong, always.

- Investment diversification will save you, even if it appears everything is going down at the same time.

- Ignore the apocalyptic predictions. Someone will benefit from making these predictions, but it won't be you!

- When markets tank, crash, correct, etc. consider the following strategies:

- Tax-loss harvesting.

- Roth IRA conversions

- Rebalancing into the pain – I.e., buy equities (Funds, ETFs) that are low.

- If you’re worried or fearful, consider revisiting your risk tolerance and investing game plan.

- Seek the counsel of trusted advisors. E.g., fiduciary, fee-only advisors, trusted family or friends.

- You must prepare for “The Crash”, before “The Crash.” Take the time to develop a well-thought-out financial plan and investment policy statement.

- Maintain Situational Awareness

- Instead of relying on YouTube or Facebook (TikTok?) for your financial education, consider taking the time to read reputable financial books that stand the test of time. These books will help you understand that market volatility is a healthy and normal part of investing.

- Read anything by Jack Bogle and William Bernstein. Their books are timeless and principle based. They may be boring to some, but if you’re not willing to read boring, timeless, principle-based books about investing then you should pay someone else to invest for you.

- Understand that there is no magic signal that alerts us of the bottom of the downturn. Furthermore, if you exit the markets during volatile times, you're very likely to miss the largest return days as well. Oftentimes the largest returns come right on the heels of the worst days.

- Instead of relying on YouTube or Facebook (TikTok?) for your financial education, consider taking the time to read reputable financial books that stand the test of time. These books will help you understand that market volatility is a healthy and normal part of investing.

Finally, remember, the only reason there is an expected investment return in the stock market is because there is uncertainty, volatility, and risk of loss. In other words, if it were a smooth elevator ride up, there would be no reward.

Sources:

1https://blog.padi.com/18-things-dangerous-sharks/

2Ibid

3Ibid

4https://www.putnam.com/literature/pdf/II508-c7166a52bb89b4621f3d2525199b64b.pdf

{kind=link}